Oil Price Forecast – October 2020

by Fergus Robson, OPC Economist & International Business Director

Our Last Prediction

In January of this year, OPC took the view that 2020 oil prices would remain at around USD 60/bbl. We estimated the impact of the virus at c. USD 3/bbl and based this upon a short-term reduction in Chinese oil demand. Back in January, this seemed reasonable and in line with most expectations – oil demand remained strong and growing, supply was well balanced, and the S&P 500 continued on its bull run from its November 2018 lows.

And then it lost 32% in the month February to March.

For Brent crude, prices fell from c. USD 60/bbl to c. USD 20/bbl over the same period – a fall of around 66% – helped along by unilateral oil price cuts and production increases by Saudi Arabia and the economic impact of shutdowns in response to the virus.

Read the Contract

We also failed to predict WTI May ’20 futures contracts trading at a negative USD 37.63/bbl on April 20th. In all likelihood, our lack of foresight was because we’d read and understood the contract specifications which demand the holder of the future at expiry (2.30 PM 3 business days prior to the 25th or 4 business days if the 25th is a weekend) take physical delivery:

“SETTLEMENT METHOD: DELIVERABLE

DELIVERY PROCEEDURE: Delivery shall be made free-on-board (“F.O.B.”) at any pipeline or storage facility in Cushing, Oklahoma with pipeline access to Enterprise, Cushing storage or Enbridge, Cushing storage.

Delivery shall take place no earlier than the first calendar day of the deliver month and no later than the last calendar day of the delivery month.”[1]

Owing to the economic impact of the virus on the economy, with aviation, travel and industrial demand collapsing (the US department of transport statistics show a 43% fall in daily trips undertaken between the end of February and the end of March) and storage at Cushing entirely contracted to producers and physical traders, many financial traders were left scrambling to offload their contractual commitment to take physical delivery of 1,000 barrels of oil per contract held. Reuters quoted a storage broker as saying:

“I never been contacted by as many hedge funds as I did yesterday looking for storage. I had dozens of emails and phone calls from hedge funds, they never really thought about the aspect of the physical delivery”.[2]

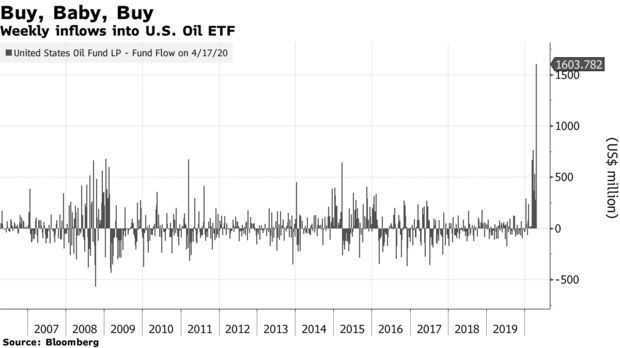

Analysis from Bloomberg suggests that a significant volume of retail money went into ‘oil prices’, with a fifth of all May ‘20 futures being held by an ETF (exchange traded fund) on the 17th April[3].

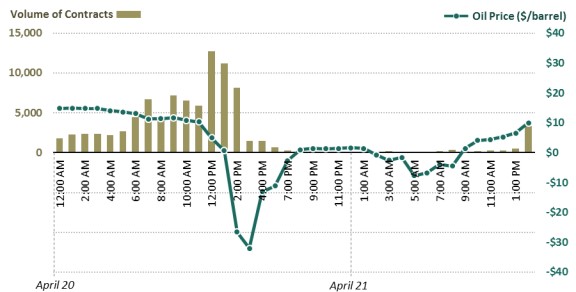

The April 20th hourly chart for May ’20 futures illustrates how the remaining contract holders liquidated at any price in order that they did not have to take physical delivery of 1,000 bbl oil per contract held. At this point, the WTI futures contract became a storage price rather than an oil price:

Brent and other benchmarks were not affected by the situation within the WTI contract as they allow financial settlement:

“The ICE Brent Crude futures contract is a deliverable contract based on EFP delivery with an option to cash settle against the ICE Brent Index.”[1]

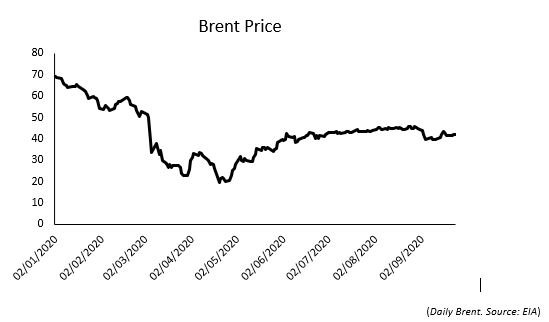

Q1 – Q3 Brent

Starting the year strongly at around USD 65/bbl, Brent closed Q3 at around USD 40/bbl, but not before it briefly dipped below USD 20/bbl.

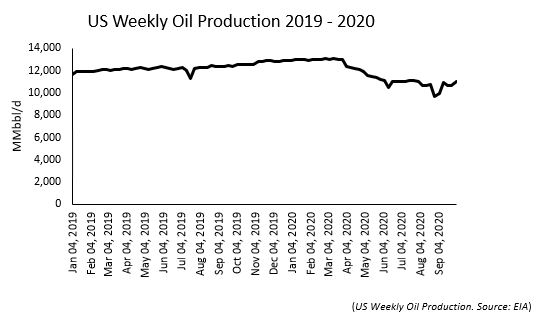

Prices rebounded in June following significant OPEC+ cuts (up to 9.7 MMbbl/d in May and June and 7.7 MMbbl/d onward), and both the USA and China taking advantage of low oil prices to refill their respective strategic petroleum reserves. Since June, Brent has remained rangebound at USD 40 – USD 45/bbl. US oil production has also fallen in reaction to the oil price:

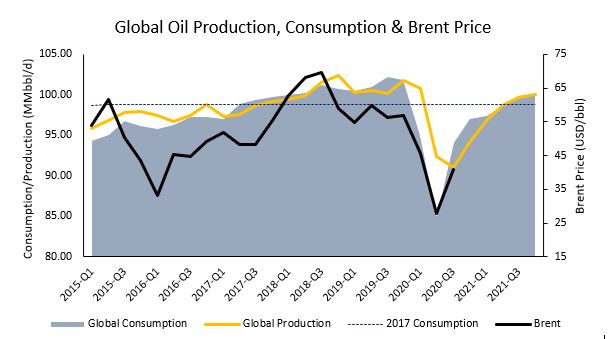

Fast forward to October and the impact on demand has become clearer, with the EIA forecasting a reduction in demand of 8.6 MMbbl/d 2019-20, from 101.4 MMbbl/d (2019) to 92.8 MMbbl/d[1]. 2021 forecast is 99.1 MMbbl/d; 2.3% lower than 2019 as recessionary factors continue to have an impact. Whilst this sounds severe, oil demand is predicted to fall to 2013 levels for 2020 and to grow to 2017 levels next year:

Of course, the above demand estimates need caveated by the unknown quantum of the global recession; particularly in western economies who have suffered unprecedented reductions in GDP. With unemployment tending to be a lagging indicator and monetary policy having a 6 – 18 month period to take effect, the economic outlook is very uncertain. How this will impact oil demand remains to be seen, with sectors such as aviation seeming unlikely to recover soon but somewhat counter intuitively used car prices increasing substantially; with the US CarGurus index showing an increase of 7% year-on-year and a similar trend in the UK.

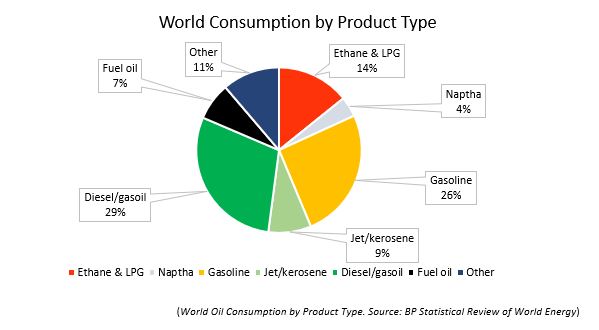

2019 oil consumption by product type is presented below:

Given what has happened in 2020, it is very difficult to say with any certainty what demand will look like by the end of the quarter let alone by the end of 2021, however, demand is recovering from its Q2 low and markets are reacting. Exploration spending has been significantly reduced, layoffs and consolidation is occurring and high-profile bankruptcies in the upstream and service sector such as Chesapeake, Denbury Resources and Noble Corporation have occurred.

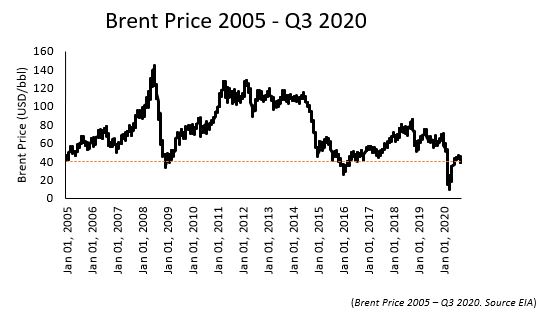

USD 40

Taking a look at oil prices over the past 15 years, a clear floor has been established at USD 40/bbl, with prices never remaining below this level for more than a month or so:

Also noticeable from the above chart is the periods of relative stability following significant market movements.

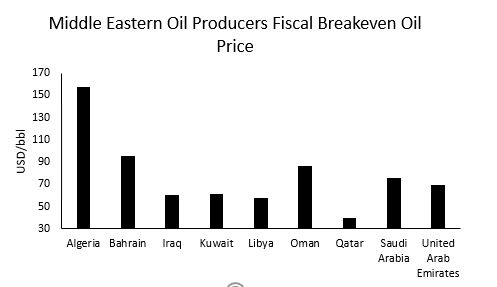

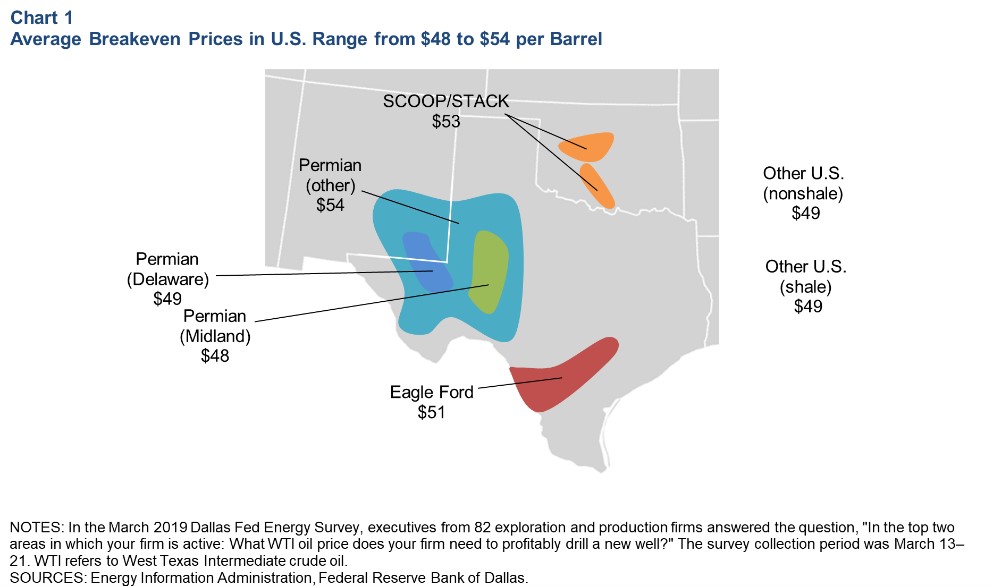

Given that the majority of producers require oil prices at or above USD 40/bbl to breakeven, and that project sanction is almost impossible below USD 40/bbl, on a supply side, the market should continue to defend this price level as a floor. OPEC+ seem committed to defending prices as evidenced by their actions over the summer. Middle Eastern producers continue to have very high fiscal breakeven levels (with Saudi, Iraq requiring prices in excess of USD 60/bbl) and US producers in general requiring oil prices to exceed USD 50/bbl for additional development to occur:

The key question is demand, but this is expected to return to 2017 levels by 2021. Clearly, given what has happened to demand Q2 – Q3 2020, there are substantial stocks within the system that will persist for months, limiting upside potential for the oil price.

OPC Oil Price Forecast

OPC forecast the oil price trade around an average of USD 40/bbl Q4 2020 – Q1 2021.

Average of $40

Fergus Robson is the International Business Director and Petroleum Economist at OPC. He has 15 years’ experience within a range of roles in the oil and gas industry, initially in commercial operational roles and moving into financial and strategic consulting for upstream operators and financial institutions

Call: +44 20 7428 1111

Email: london@opc.co.uk

Agree or disagree? Comment on OPC LinkedIn

[1] https://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude_contract_specifications.html

[2] https://www.reuters.com/article/us-global-oil-usa-storage-idUSKCN22332W

[3] https://www.bloomberg.com/news/articles/2020-04-20/oil-worth-less-than-nothing-points-to-a-deepening-global-crisis