Max Richards, Energy Transition Services Lead, OPC, outlines the realities of commercialising CCS from the perspective of an independent operator and provides some insights from a non-early mover.

The majority of our major clients are small- to medium-sized independent oil and gas companies centred on one or two major assets. Our focus in supporting our clients is usually on two key objectives: maximising value and developing technical expertise. Achieving these goals means aligning to key principles; positive cash flow, realistic long term objectives, and focusing on core business activities. This is where the first obstacles to Carbon Capture and Storage (CCS) appear. Our experience working alongside our clients is that there is a large amount of ambiguity in addressing the above and key questions always arise.

How do you make money from CCS? Will CCS be supported by the regulator and the governments over the lifecycle of our assets? How can I get involved? There are a number of anxieties our clients have – as well as a desire not to be left out given the quickly-evolving future of CCS and that information is hard to discern.

In our most recent CCS project as a part of a larger technical study examining a client’s reservoir storage capacity, injection profiles, and geomechanics we sought to understand what modifications would be needed to inject CO2 at a sustained rate (1Mt, 3MT and 5MT/PA). This included the facility modifications and the associated CAPEX and OPEX costs.

In conjunction with well-developed theoretical and practical CO2 storage capacity calculations, we were able to accurately estimate the cost per tonne of CO2 injected and stored into the reservoir over 50 years. Armed with our injection costs OPC ran a number of economic projection scenarios to estimate the price to charge potential customers for using our client’s reservoir. Job done!

The more seasoned amongst us will know that is it unfortunately not as simple or straightforward as that. There are several moving parts that need to be constrained and understood before going to market. The Energy Transition team at OPC made the client aware of this, with further research and conceptualisation required.

This was a journey that we undertook together; to translate business models and regulatory dependence into easily digestible concepts, demystifying commercialisation routes, and discerning ‘what slice of the pie’ each stakeholder in the CCS value chain will receive (capture, dehydration, compression, transport, utilisation, and storage).

In this article, we will outline the realities of how to commercialise CCS from the perspective of an independent operator whilst remaining true to our principles of maintaining positive cash flow and aligning to long term objectives of relevance and remaining in touch with reality. It must be stressed that this article reflects our interpretation of government policy and the market.

It should not be taken without a pinch of salt. Of note is that the work that was completed was an initial study to understand key concepts, constraints, and opportunities. OPC focuses on developing the knowledge and technical expertise to enable our clients to control and understand the narratives of the energy transition running through the global oil and gas industry for their advantage.

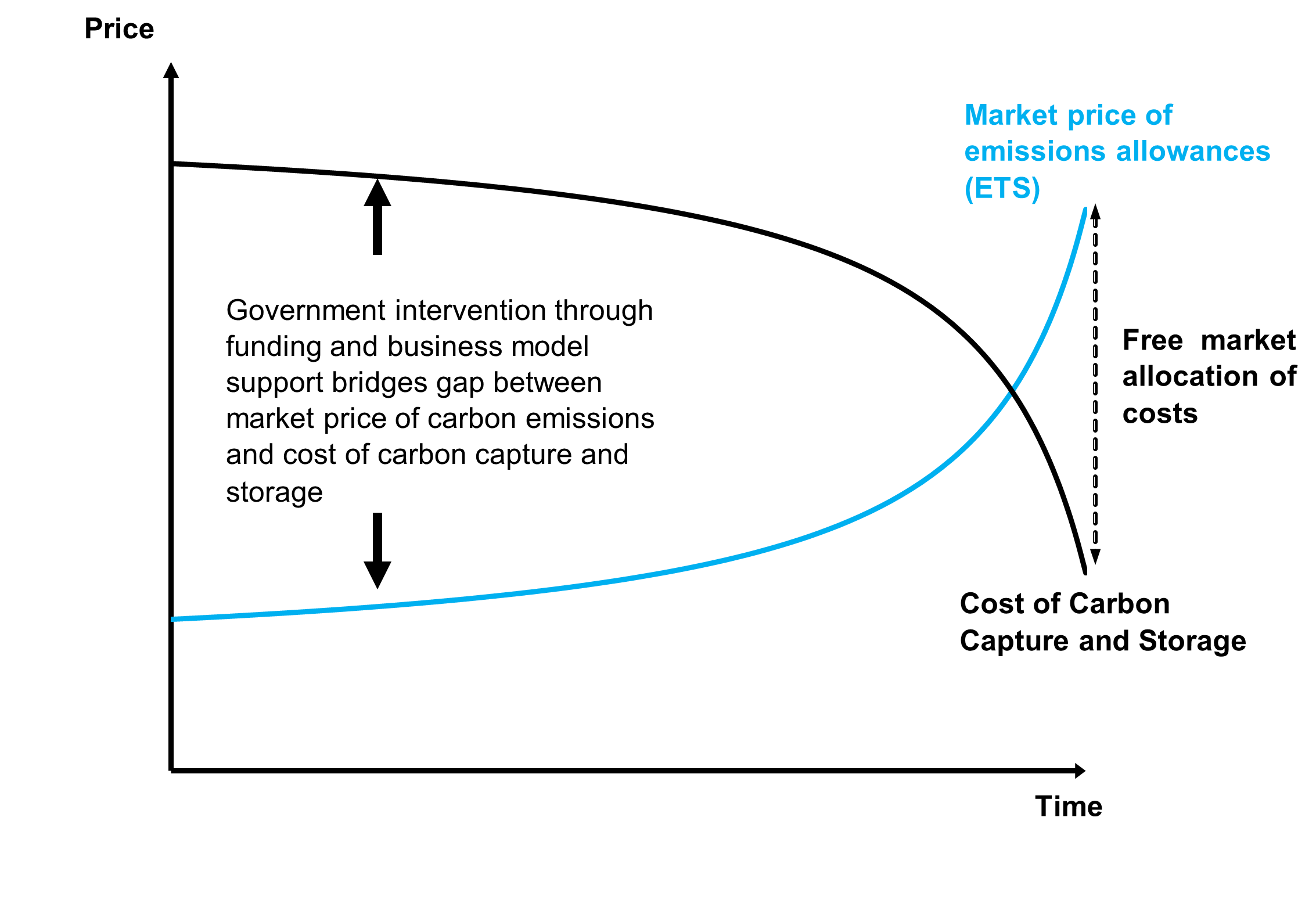

Figure 1 – Illustrative example of how government intervention will underpin market failings of CCS until cost of carbon capture and storage is lower than the market price of emission allowances. Adapted from Industrial Decarbonisation Strategy (BEIS; March 2021)

The Cost of CO2

The Cost of CO2 In January 2021, the UK Emissions Trading Scheme (UK ETS) replaced the EU ETS, placing a cost on greenhouse gas (GHG) emissions across energy-intensive industries. These markets seek to price the externalities of polluting CO2 more accurately by forcing energy-intensive industries to purchase emissions allowances (1 ETS = 1 tonne of CO2e) from the ETS.

The ultimate objective is to bridge the gap between the cost of emission reduction and the market price of emissions allowances so that a free market can then determine the most efficient pathways to decarbonisation. The development of a free market is inherently reliant on the price of polluting CO2 being sufficient to drive polluters to invest in CCS and emissions reduction technology.

In October 2021 the current price for one EUA (allowance) is hovering around €58 and in the UK £58, lower than the cost of CCS. Many believe this price is still too low to reach 2030 and subsequent targets across the Europe as solutions such as CCS are still in the €100 to €200 per tonne range. Uptake of CCS will depend on the carbon price and the price of source-to-sink technologies. If the price per tonne of CO2-avoided by CCS is lower than the carbon price, then CCS may begin to be commercially attractive.

In the immediate future, the carbon price is not sufficient to drive markets to begin capturing and storing CO2 without market intervention by governments. Many of the industries seriously considering CCS such as steel and cement are ‘hard to abate,’ meaning pathways to reduce emissions through electrification and use of low-carbon fuels are particularly challenging. In order to support these essential industries and prevent the acceleration of emissions costs, CCS can be deployed to keep industry competitive whilst minimising emissions. But as the price of pol[1]luting remains too low; government intervention is required (see Figure 1).

Carbon Capture and Storage Clusters

In December 2020 the Department for Business Energy and Industrial Strategy (BEIS) outlined their position on the commercial business model describing CCS cluster sequencing and Transport & Storage (T&S) business models. These were designed to incentivise deployment of carbon capture technology for industry to help overcome a number of different market failures and barriers to entry that prevent industry from securing investment needed to start the low carbon transition. For ‘first of a kind’ projects, BEIS expect the model to cover operational costs, T&S fees and a rate of return on capital investment, with an element of capital co-funding for initial projects.

In October 2021 it was announced that the government would be spending £1 billion to support the development of two CCS clusters and T&S networks, East Coast & HyNet. Industrial hubs and CCS clusters are the preferred business model being adopted worldwide through the utilisation of a Transport & Storage (T&S) network. In this business model, heavy industries such as cement, steel, and fertiliser production which exist in industrial clusters are connected to a T&S network.

This allows multiple sources of CO2 to access a common CO2 T&S infrastructure. This significantly reduces the unit cost of CO2 storage through economies of scales and offer commercial synergies that reduce investment risk. T&S networks also reduce cross-chain risk by creating multiple customers for the operators of CO2 T&S networks, including CO2 arriving from outside the local cluster such as via ship. Under this model ‘users’ of the T&S network will pay a fee. As these networks will be inherently monopolistic, they would be heavily regulated by governments like other monopolistic networks such as rail, water, and gas. We will go into this in further detail in the next section – bear with us, it gets quite complicated.

Figure 2 –The White Rose CCS Project (2014) would have been the first coal-fired power plant to demonstrate the use of CCS.OPC provided support in reservoir simulation and modelling for long term carbon injection and storage project.

The reason ‘clusters and hubs’ are being developed is that they overcome one of the key risks associated with CCS projects – cross chain risk. Previously projects such as the UK’s CCS competition (White Rose, which OPC worked on; Figure 2) attempts were made to capture CO2 from a single source and inject and store into a single sink. This is referred to as a disaggregated business model such as Sleipner and Gorgon. This model ultimately led to higher costs of capital and higher project costs.

So far, I’ve tried my best to give a good overview of the main commercial levers incentivising CCS, the avoidance of an emissions bill and to keep industries competitive. We roughly understand the drivers of market intervention and what is expected from policy makers, what do the proposed state supported business models look like?

Transport & Storage Business Models

Supporting the development of the two CCS clusters BEIS has outlined the proposed business models for the provision of Transport and Storage companies, referred to as ‘TS&Co’. These commercial entities are joint ventures (JV) which will construct, manage, and decommission the transport of CO2 from ‘users’ to an appropriate storage reservoir via a network.

The TS&Co will be the asset owner and the system operator. The aim of the TS&Co business model is to support the development of CCS clusters while managing the key risks associated with large infrastructure projects which are naturally monopolistic. BEIS guidance to date on how these business models are designed is constantly changing, and certain aspects remain ambiguous.

To simplify as much as possible, the revenue generation of the TS&Co will be set by strict government policy through defined phases.

Essentially government support will be greatest during the first phases of deployment and will taper away as clusters are anticipated to become independent from support. In the subsequent regulatory periods, the regulator (the government) would design the Economic Regulatory Regime (ERR), covering allowed revenues and any other incentives/penalties. In effect the regulator would be similar to that in sectors currently subject to independent economic regulation such as electricity, gas, water, telecoms, and transport. The business model does not cover the supply of CO2 via non-pipeline transportation, though it does indicate that this subject will be dealt with in subsequent policy updates. To summarise, the CCS business will be treated like a waste disposal with dictated utility-esque margins.

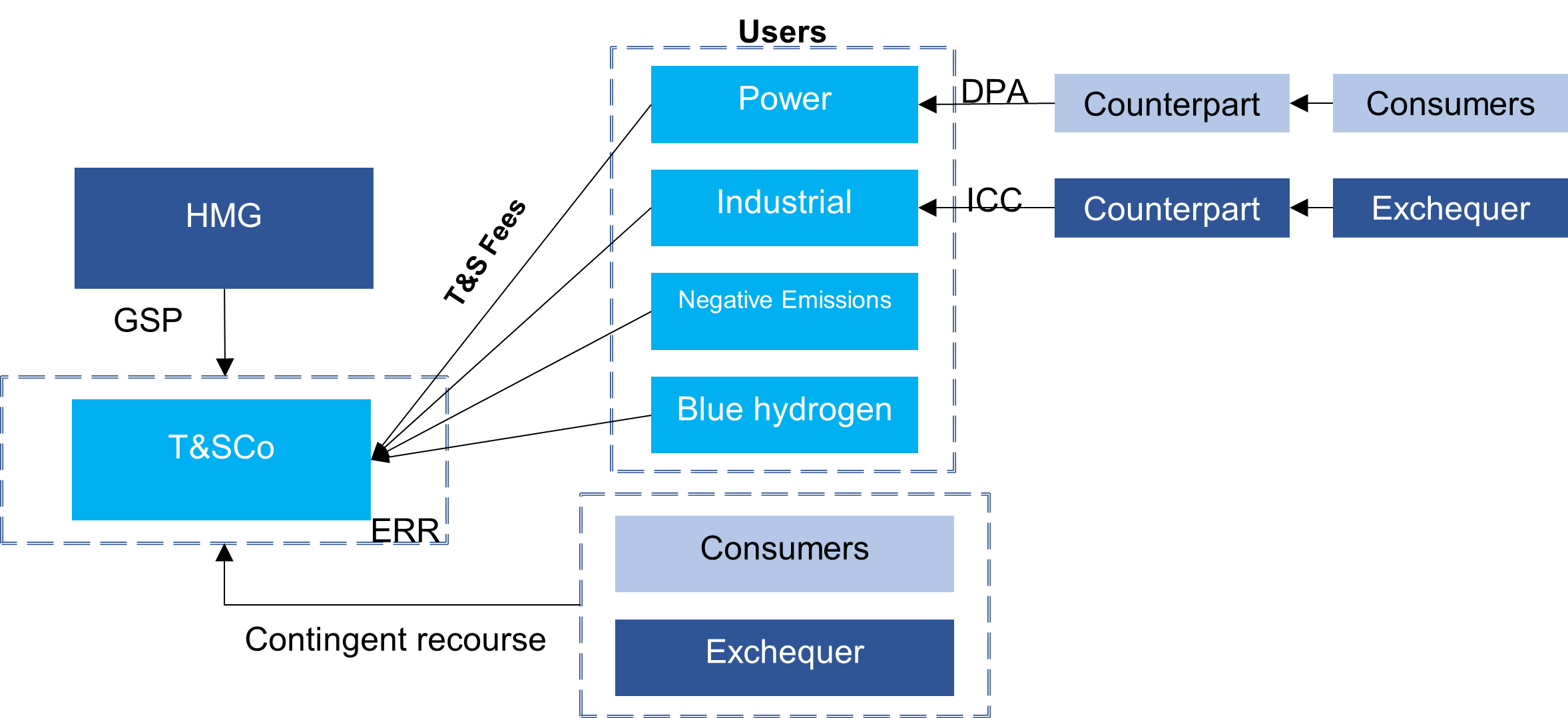

Figure 3 – Diagram of revenue stream model for the TS&Co. HMG will support the development of the T&SCo via Government Support Packages (GSP). The T&SCo will be governed by an Economic Regulatory Regime (ERR). T&S fees will be generated from expected users of the network – power stations, industrial facilities, negative emissions technologies, and blue hydrogen. Power users will be subsidised by Dispatchable Power Agreements (DPA), industrial users via Industrial Carbon Capture (ICC) agreements.

So, who’s paying for it?

Whilst the BEIS T&S business model covers the organisational structure by which the T&SCo will be regulated it does not cover the revenue sources. Under the T&SCo revenue model, revenue will be generated by users under a ‘Users Pays’ model. Within this agreement users of the T&S network will pay fees reflecting the magnitude of their use of the network. Elements of fees would be connection, capacity, and volumetric fees. Under this agreement the T&SCo would also have ‘contingent recourse’ to consumers and/or taxpayer support to ensure the revenue stream from users is predictable and robust from a financial perspective. It is outlined in Figure 3.

What does it all mean for me?

One thing is for sure, the economics of CCS are nowhere near as glamorous to that of Oil and Gas. Returns are as a utility and it at this current point in time seems like a risky business to be in, subject to the discretion of governments for financial support. Costs along the chain are highest when capturing CO2 and often are as much as 90% of total costs.

Dehydration and compression of CO2 costs around 5-15%, transport depending on pipeline, shipping, and length can be as low as 5% and up to 20%. Storage incidentally, and the bit that the upstream oil and gas industry will likely be most involved can be very cheap, as low as 2.5% of costs. Costs change by a large margin depending on the specific case being examined.

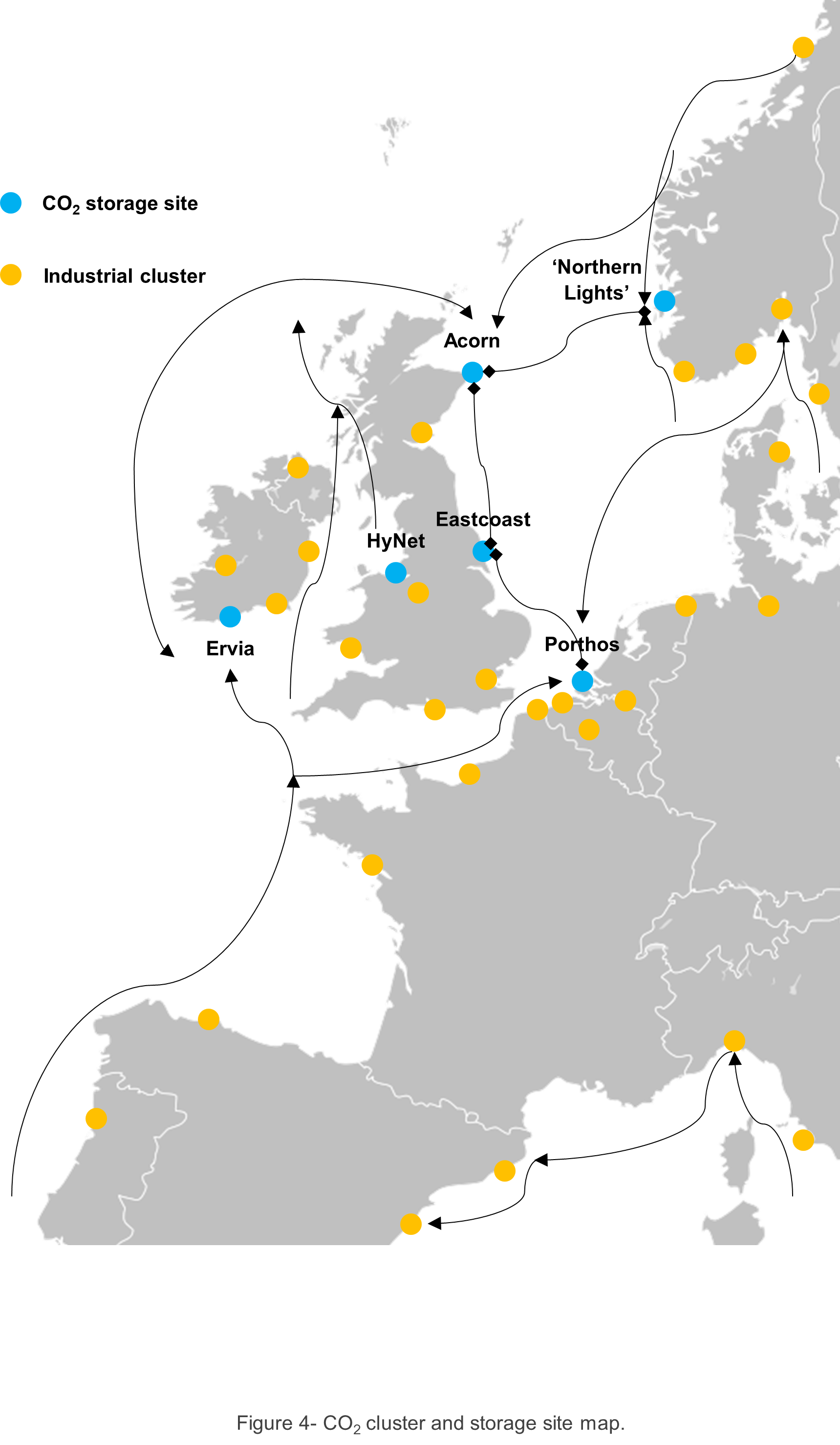

CCS projects globally are focusing on developing ‘low hanging fruit’, clusters optimally aligning a combination of CO2 source and transport network scalability, and access to optimum storage sites (see Figure 4). When those storage sites are filled with CO2 the next best reservoir will be utilised. This will be the opportunity for new parties to enter the market, subject to the success of current projects and net-zero goals.

If you own and operate an asset in the North Sea and you repurpose as a storage site, decommissioning and abandonment costs will be significantly less. And you may be able to generate revenue for another 50 years. For independent oil and gas companies who may not have a 50-man strategy team trying to predict the future, CCS may seem a bit a long shot. But it also may be an opportunity to safeguard revenues and prevent stranded assets.

Figure 4- CO2 cluster and storage site map.

Please contact Max Richards for more information.

Max Richards

Energy Transition Lead

+44 20 7428 1111

max.richards@opc.co.uk