North African Petroleum Systems – attractive future potential

by Robin Crawford, Senior Consultant Geologist

Exploration in North Africa began in the early 1900s but really took off in the late 1950s and the 1960s when a large number of the major fields of Algeria, Libya and the Egyptian Gulf of Suez were found. The region continuously increased production throughout the 1960s and 1970s and has maintained significant output to the present day. There have been conflicts that have interrupted investment but the region has always kept the industry interested.

In the 1990s the Algeria Berkine trend of 6-8 billion barrels of oil equivalent (bboe) was found and in the 2000s the Nile Delta with its huge gas potential came to the fore. There is still conflict in the region. Libya has not yet recovered from its independence from 42 years of dictatorship. The region still holds the industry’s interest with the potential for growth in conventional resources in all of the countries and for the huge potential in shale oil and gas in the area.

When the industry refers to North Africa we generally mean the countries of Morocco, Algeria, Tunisia, Libya and Egypt. To understand why North Africa is important and to understand how it offers such huge potential it is always good to get an understanding of scale. The land area of North Africa is equivalent to almost three quarters of the land area of the continental USA. Texas (always a good measuring tool for the oil industry) would fit into Algeria alone more than three times. The area is vast.

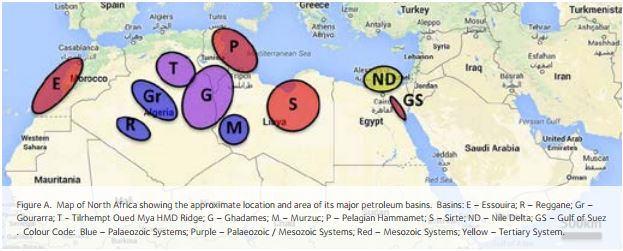

The map above shows the petroleum basins of North Africa, their approximate location and area. Resources of approximately 150 bboe have been discovered and partly produced in these basins. In 2013 the USGS World Petroleum Resources Project published Yet to Find (YTF) numbers for the area of an additional 82 bboe of risked recoverable conventional resources comprised of 19 billion barrels of oil and 370 Trillion Cubic Feet (TCF) of gas. In 2011 the US Energy Information Administration estimated risked recoverable resources of shale gas from the area of a further 550 TCF. They did not estimate the potential for associated condensates and shale oil, which will be considerable.

Huge numbers by any one’s standards and close to one of the world’s largest markets. Two gas pipelines to Spain and Italy have been built in the last 15 years to add to the existing line to Italy. Liquefied Natural Gas (LNG) is shipped from Algeria around the world including the UK. North Africa gas is hugely important to Europe to provide competition and diversification of supply. So why is North Africa so prolific in hydrocarbons? It comes down to two factors: multiple good to excellent quality source rocks, and efficient petroleum systems.

The quality (thickness and richness) of the North African source rocks is what drives the quality of the North African petroleum system and therefore the exploration opportunity. The Palaeozoic Silurian and Devonian source rocks of North Africa are some of the best in the world. Luning (2000, 2003) has written at length about them. The organic content of both intervals has been measured in excess of 20%. The source intervals have widespread preservation and reach thicknesses in excess of 80m (Silurian) and 200m (Devonian) in Algeria. The Mesozoic and Tertiary source rocks of the Pelagian, Sirte and Nile Delta are also good to excellent quality and can be several hundred metres thick (Pelagian and Sirte) with TOC’s up to 6% (Baric 1996, Mejri 2006).

If source rock quality is the most important factor to drive the quality of a petroleum system then in North Africa, timing of generation, expulsion and migration is a close second. Late is good, allowing time for the emplacement of reservoirs, seals and traps. In North Africa most of the basins have late generation and migration or an element of it. The Eastern Algeria basins, the Pelagian and Sirte basins have been in a generation and migration phase for most of the Tertiary and part of the Late Cretaceous period – the last 60-80 million years. This is long after the deposition of the prolific Triassic reservoir with its Triassic Jurassic evaporate super-seal in Algeria and mostly after the deposition of the late Cretaceous and early Tertiary reservoirs and seals of the Sirte and Pelagian basins.

The Palaeozoic systems (e.g. Ghadames) are generally less efficient than the Mesozoic systems (e.g. Sirte) because they have an early phase (375 to 300 mybp) of generation and migration. The products of this phase are lost at the Hercynian uplift and erosion (320 to 250 mybp). In these systems the hydrocarbons found today are those generated in the late phase (80 mybp to present day) of generation and migration. This is with the exception of the Algeria Reggane and Gourara basins where the source rock is fully converted pre-Hercynian times and the only hydrocarbon found today is dry gas associated with the last phase of migration as the source rocks are uplifted and decompacted to release trapped methane.

The USGS study of risked YTF suggests that there is more than half as much again to be found and produced. Over the last 5-8 years onshore exploration 3D has become the order of the day and as this becomes cheaper and the quality of image improves then the more subtle traps will be imaged to release these hydrocarbons. The EIA study highlights the huge potential for shale gas. Exploration companies are already active in Tunisia for shale potential and the Tunisian authorities are reviewing contract changes to accommodate shale projects. Shale exploitation is the next phase if the rocks are right and the industry can overcome the considerable operational challenges. North Africa remains attractive to the industry and still has much of its energy prize to give up.

TECHNICAL WHITE PAPER – December 2014

By Robin Crawford, Senior Consulting Geologist

Dr Robin Crawford is a Consulting Geologist who is recognised as a leading expert on the petroleum geology of North Africa. Robin has 30+ years’ experience with Amoco and BP in the industry and has worked mostly North Africa for the last 20 years.